[ad_1]

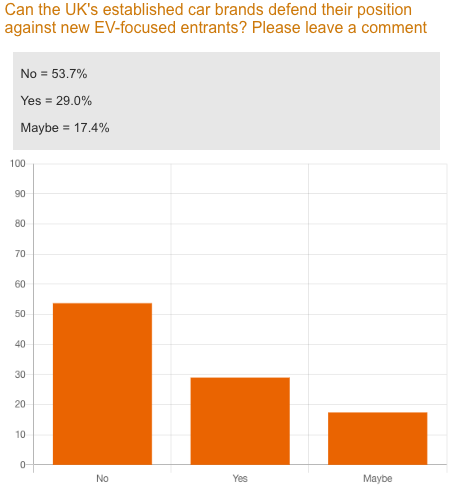

Over half AM’s readers (53.7%) consider the UK’s established automotive manufacturers will battle to defend their market share towards new electrical car (EV) focussed entrants.

New Chinese language manufacturers like BYD and GWM Ora have already launched within the UK and different new entrants like Omoda, Nio and B–ON are all lining as much as kick-start gross sales throughout the subsequent 12 months.

Nonetheless, practically a 3rd (29%) of AM’s ballot respondents are extra optimistic about established authentic gear producers’ (OEMs) possibilities to defend their place.

The remaining 17.4% have been undecided, with some citing that there are such a lot of elements at play that it’s tough to foretell what is going to occur or whether or not sure OEMs can be pushed out of enterprise.

Robert Forrester, Vertu Motors chief government, is definitely within the optimistic camp, telling AM in Might that: “All of the producers we signify have clear EV methods and to say the Chinese language manufacturers are the one ones which might be going to capitalise on EV is nonsense.”

Nonetheless, a few of the nameless feedback on the ballot consider in any other case.

One respondent mentioned: “There are such a lot of elements to think about, not least the supply of all supplies required for battery manufacturing and on the required scale going ahead which is already tough.

“The Chinese language OEMs seem to have this coated in abundance. European producers have to unfold their base to incorporate a mixture of inner combustion engine, electrical/hybrid and maybe most significantly hydrogen.”

One other respondent described the established OEMs as “letting their networks down by shifting to company”, which they consider the Chinese language manufacturers will capitalise on by sticking with a franchised vendor mannequin.

BYD is concentrating on to increase to a community of 100 franchised sellers by 2025, Ora needs to ascertain 13 places earlier than the tip of 2023, Omoda needs over 50 dealerships within the UK earlier than its February 2024 launch and German electrical van model B-ON is wanting to ascertain 25 places earlier than 2024.

However not each new entrant is seeking to associate with franchised sellers, with China’s premium focussed EV model Nio seeking to mirror Tesla’s method (ET5 Touring mannequin pictured beneath) by getting into the UK with a direct to client digital-first mannequin.

One other AM reader mentioned altering client attitudes to vehicles and mobility on the whole will play in favour of the brand new disruptor manufacturers.

They mentioned: “The final commoditization of the sector, lack of brand name funding and differentiation from OEMs will solely speed up this pattern, particularly within the mid-market quantity sector.”

Pricing may even be an essential issue, one thing that MG has capitalised effectively on to ascertain itself shortly as a great worth proposition within the EV area.

MG has grown by 58% within the first six months of 2023 and brought over 3% market share within the UK.

An AM reader mentioned: “If the brand new Chinese language manufacturers and disruptors can launch merchandise with wise pricing this can put strain on the established manufacturers.

“Many mainstream EV costs are already in status worth territory and out of attain of most individuals.”

This doesn’t appear to be the present technique of manufacturers like Ora, which is priced from £31,995, which is comparative somewhat than undercutting fashions just like the Vauxhall Corsa-e.

Likewise, the BYD Atto 3 is priced from £37,695, which is analogous to one thing like a Kia Niro EV.

One of many AM ballot respondents believes OEMs will defend their place and the established OEMs are additionally very EV-focussed.

They mentioned: “The established OEMs have UK market expertise, technician information and analysis and growth budgets to compete alongside any new entrants to the market.”

Established OEMs also can shield their market share by having a “sturdy ecosystem of assist for purchasers of recent EVs”.

One ballot respondent mentioned: “Help with recommendation on adoption, house charging and EV possession will shortly grow to be a USP for them within the face of recent entrants who could have but to ascertain partnerships in these areas.

“The extra they’ll assist new EV prospects with their transfer to electrical, the extra probably that buyer can be keen to buy from them now and going ahead.”

[ad_2]