[ad_1]

Optimists will level to the truth that June 2023 was the eleventh consecutive month of development, with the market up 18.4% YTD. Pessimists will level out that, within the first half of the 12 months, the UK market was nonetheless 27.7% beneath the place it was 5 years in the past.

In the meantime, the SMMT is at the moment forecasting a complete determine of 1.83 million for 2023, which is about the place the market was in 1994, writes David Francis.

At a producer stage, the most important improvement YTD has been VW retaking the No. 1 spot from Ford. It appears unlikely that VW will relinquish its place any time quickly, as Ford ended manufacturing of the Fiesta in June, with the Focus on account of comply with by 2025.

With a slim crossover-focused automotive vary (a few of which can be based mostly on VW platforms), it’s arduous to see how Ford can compete with VW’s “entry all areas” 16-model line-up.

The truth is, third-placed Audi is extra prone to catch VW than Ford, given long-term developments – though whether or not that will be allowed by the VW hierarchy is one other matter. It’s fascinating to notice, nevertheless, that the A4 E-tron has offered extra thus far this 12 months than any electrical VW.

It’s due to this fact no shock that there was an emergency facelift of the pretty lacklustre ID3. This was named because it was to be the third seminal VW after the Beetle and the Golf: thus far its efficiency appears to be like extra new Jetta than new Golf.

Kia has slipped behind Audi, and is now solely simply forward of Toyota, which sits in fifth place. Nonetheless, Kia’s market share of over 6% remains to be an excellent determine for a producer that, 20 years in the past was an economic system model with minimal market consciousness.

That’s each an inspiration and a warning – you’ll be able to wager the Chinese language manufacturers have been learning Kia’s UK success very fastidiously.

Toyota’s progress has some parallels with Kia – it has had good development in recent times, however has seen a fall in market share this 12 months. As Asia’s pre-eminent automotive producer, it definitely gained’t be joyful about being outsold by a relative upstart from South Korea. The most important distinction is that Kia has among the best ranges of battery electrical autos within the business, whereas Toyota has struggled to even get its first BEV (the BZ4X) to market: the primary 2700 vehicles made needed to be recalled for wheels probably falling off (the information headline wrote itself).

Toyota’s progress has some parallels with Kia – it has had good development in recent times, however has seen a fall in market share this 12 months. As Asia’s pre-eminent automotive producer, it definitely gained’t be joyful about being outsold by a relative upstart from South Korea. The most important distinction is that Kia has among the best ranges of battery electrical autos within the business, whereas Toyota has struggled to even get its first BEV (the BZ4X) to market: the primary 2700 vehicles made needed to be recalled for wheels probably falling off (the information headline wrote itself).

Behind Toyota (and uncharacteristically adrift of Audi) is BMW. Its market share of 5.5% YTD is its lowest for a few years. One of many predominant causes is a 2.5% fall in 3 Sequence gross sales – the automotive that was historically BMW’s greatest vendor is now outsold by the 1-Sequence, 4-Sequence and 2-Sequence.

As regards to as soon as best-selling fashions, seventh-placed Vauxhall is battling the brand new Astra. It’s nonetheless not even within the High 10 C-segment hatchbacks (behind the Mini Countryman) or the High 25 C-segment fashions if crossovers are included. Certainly outselling the Mazda CX-5 shouldn’t be too huge an ask for a mannequin that used to battle for section management?

As regards to as soon as best-selling fashions, seventh-placed Vauxhall is battling the brand new Astra. It’s nonetheless not even within the High 10 C-segment hatchbacks (behind the Mini Countryman) or the High 25 C-segment fashions if crossovers are included. Certainly outselling the Mazda CX-5 shouldn’t be too huge an ask for a mannequin that used to battle for section management?

The segments below scrutiniy

The segments below scrutiniy

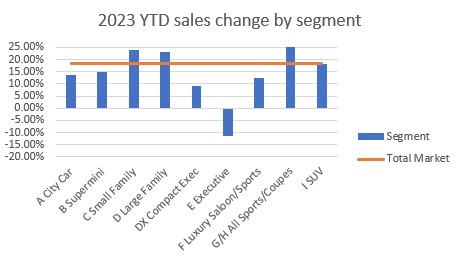

At a section stage, it’s a story of ever-greater focus, no matter whether or not the market is examined by bodystyle or automobile measurement.

For the primary time, over half of complete gross sales have been crossovers/SUV. C-segment vehicles (the main exponent having morphed from the Focus to the Qashqai) took a document 38.7%, whereas B-segment superminis (now led by the Ford Puma) took 31.7% – not fairly a document, however shut.

Premium/massive SUVs (from the Volvo XC40 upwards) took 17.9%, which meant that the three largest segments took their highest-ever mixed share of 88.2%.

The consequence was that six different segments needed to share lower than 12% of the whole market.

The largest casualty has been Govt saloons and estates, such because the BMW 5-Sequence. This section took simply 1.1% share YTD, down from 2.4% in the identical interval of 2020. May the manager saloon go the identical manner because the C-segment saloons of the Nineteen Eighties just like the Ford Orion and Vauxhall Belmont – or the way in which of the Ford Mondeo and Vauxhall Insignia of more moderen years?

With crossovers now the default selection, the place will new patrons of govt saloons come from – might the section fade away together with its, er, mature clientele?

With crossovers now the default selection, the place will new patrons of govt saloons come from – might the section fade away together with its, er, mature clientele?

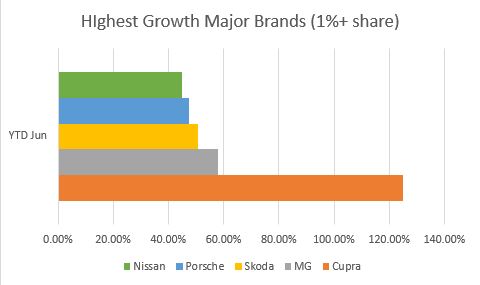

The opposite main development thus far this 12 months has been the rise of latest manufacturers – or a minimum of a few of them. Cupra has doubled its market share in comparison with the identical interval of 2022 (0.6% to 1.2%), as a classy re-invention of Seat.

Polestar has achieved the identical feat (0.35% to 0.7%), as a cooler, extra fashionable Volvo. The Polestar 2 is at the moment the second best-selling Compact Govt mannequin, behind solely the BNW 4-Sequence. It’s even outselling the Tesla Mannequin 3 which given Tesla’s distinctive charging community, is sort of a consequence.

Clearly loads of patrons favor Scandi-cool to California bombast.

It’s too early to attract conclusions in regards to the bravest new model to enter the UK market – Genesis. We are able to say it’s no Infiniti – with gross sales of simply over 800 YTD, it’s in all probability doing in addition to might be anticipated at this stage.

It will likely be fascinating to see if Genesis could make something like the identical price of progress as its Hyundai and Kia siblings.

It will likely be fascinating to see if Genesis could make something like the identical price of progress as its Hyundai and Kia siblings.

Sadly, it’s not too quickly to touch upon the destiny of some new manufacturers. DS is becalmed at simply 0.2% market share, primarily as a result of no-one appears to know what it’s for.

Lastly, in these troublesome occasions, let’s end on two optimistic tales of attainable model redemption. After 20 years of spiralling downwards, the brand new Avenger has lastly given Jeep a mannequin that would promote in first rate numbers within the UK.

In the meantime Lotus has seen gross sales enhance from principally nothing to 667 YTD. Its reinvention below Geely is underway, and we must always hope that this model, with a historical past of extra unfulfilled promise than nearly another, can lastly flourish.

[ad_2]